February 2024 – As of the close of 2022, Serbia's banking sector faced challenges amid global economic conditions. The year 2023 brought its distinct set of obstacles, with a noteworthy slowdown in global inflation compared to the last quarter of 2022. However, the undeniable focal point is the war in Ukraine, triggering a faster inflationary spiral due to increased energy and food prices.

Key mergers and acquisitions

In 2020, Komercijalna Banka, the largest state-owned Serbian bank, was acquired by Slovenian NLB Banka, leading to the merger of NLB Banka and Komercijalna Banka into NLB Komercijalna Banka. Vojvodjanska Banka was acquired by Hungarian OTP Bank, followed by OTP Bank's acquisition of Societe Generale Bank. In 2021, Direktna Banka and Eurobank merged into Eurobank Direktna, and AIK Banka acquired Sberbank Serbia, later rebranded as Nasa AIK Banka. Raiffeisen Bank in Serbia acquired Credit Agricole Bank in August 2021, renaming it RBA Bank in September 2022, with full integration anticipated by the end of Q2 2023.

Despite expectations of a temporary halt in mergers and acquisitions in the domestic banking sector in 2023, AIK Banka signed an SPA to acquire 100% of the ownership of Eurobank Direktna in February. Upon completion of the transaction, the total number of operating banks in Serbia is expected to be 20.

Serbia’s banking sector in numbers

At the end of 2022, the total number of active banks in the Serbian market was 21. Only six months later this number decreased to 20. The consolidation trend continued and financial results on the sector level in 2022 and H1 2023 insinuate the same trend for the next years.

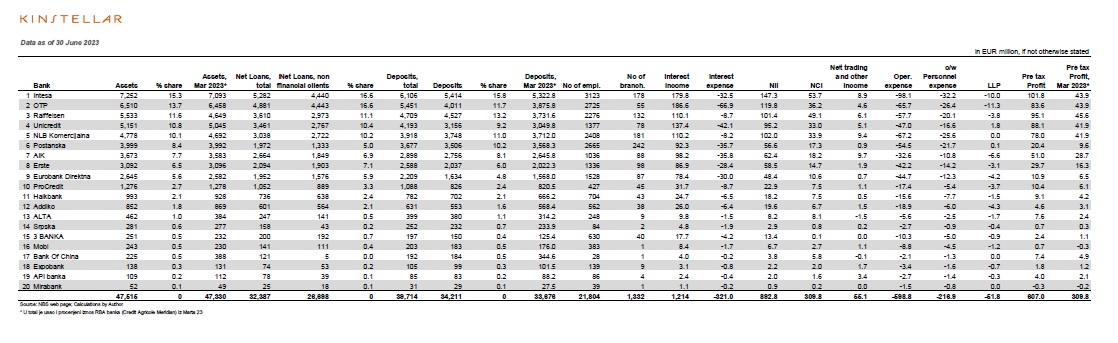

As of December 31, 2022, the sector's total assets stood at EUR 46.5 billion, witnessing an increase to EUR 47.5 billion six months later in 2023.In the first half of 2023, the top 10 banks collectively held assets totaling EUR 43.9 billion, constituting 92.4% of the sector's total assets. Simultaneously, the top 5 banks accounted for EUR 29.2 billion in assets, representing 61.5% of the total sector assets.

Notably, nine banks held a minimum 5% share of the total assets in the sector.

A very similar situation can be seen on the deposit side. The top 10 banks participated in the H1 2023 with 92.4% of the total deposits in the sector.

In terms of size measured by the number of employees, over 2000 employees on 30 June 2023, have Intesa (3123), OTP (2725), Raiffeisen (2276), NLB Komercijalna (2408), and Postanska (2665).

On 30 June 2023, the following banks had more than 100 branches: Intesa (178), Raiffeisen (132), NLB Komercijalna (181), and Postanska (242).

However, this number is progressively becoming less and less important even in jurisdictions that are lagging in digital literacy, such as Serbia.

In terms of profitability, the situation is the following. On 31 December 2022, the total pre-tax profit of all banks in Serbia was EUR 607 million out of which the first 10 banks made 93.7%. At the end of 2022, 8 banks had ROAE above 12.5%. At the same time, 9 banks had ROAA above 1.5%.

When it comes to the CIR (cost/income) ratio, 7 banks had it below 60% on 31 December 2022.

Conclusion

The years 2021 and 2022 were significantly marked by M&A activities. The same trend continued in 2023. Some of the processes have come to an end, and several mergers are still ongoing.

The market is still in consolidation mode and figures clearly show a lack of business case for several banks. Regional banking groups OTP and NLB are openly ambitious to further grow, and the same goes for domestic AIK bank. Intesa and Unicredit are still keeping up the pace with the latter group through organic growth. Erste bank officially expressed the same intentions.

Rumour has it that at least 4 banks are currently looking for the new owner in the Serbian market. So, we see similar transaction dynamics in 2024, as in previous few years.

Click on the images below to read the Serbian banking sector report or click the following links for figures as of December 2022 and June 2023.